Lodging and Cruise Forecast

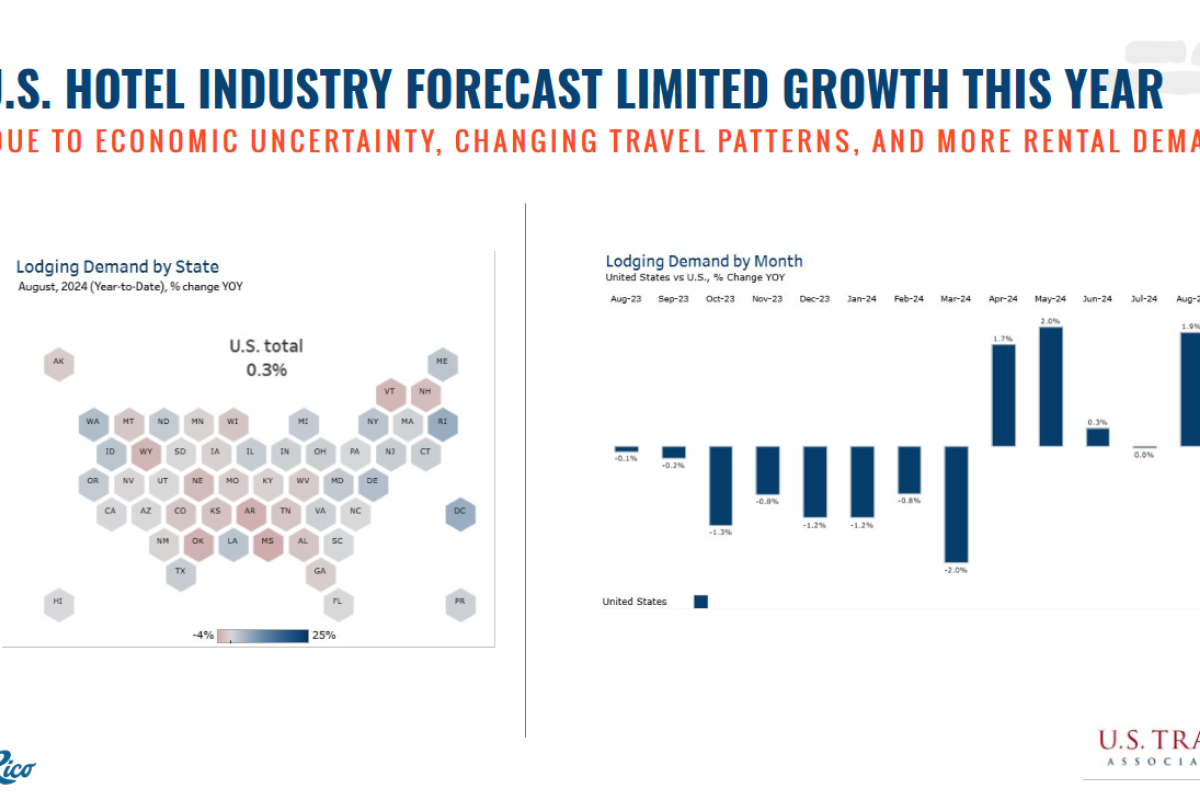

According to the Global Hotel Industry Outlook prepared by industry partner Skift, the U.S. travel industry faces moderate pressures due to economic uncertainty, shifting travel patterns, and increased competition from alternative accommodations. CBRE, a global leader in commercial real estate services and investments, revised its forecast for U.S. revenue per available room (RevPAR) growth to just 1.2% for the entire year. Back in February, they projected 3% growth, but this was reduced to 2% in May.

Urban and airport hotels are expected to outperform, while resort locations underperform relative to the boom they experienced after the pandemic. The limited supply of new hotels is helping to maintain prices, while some consumers are opting for short-term rentals due to cost, location, or the need for more space. According to the U.S. Travel Association, year-to-date U.S. hotel demand has grown by 0.3%, with the Washington D.C. area seeing the highest growth at 5%.

Locally, the lodging market reflects many of the national trends identified by CBRE. From January to August, hotel demand grew by 1% compared to the same period in 2023. Average hotel rates have risen by 2%, while the number of available hotel nights has increased by 4%. Hotel RevPAR has decreased slightly by 0.4%. Meanwhile, short-term rental demand surged by 13%, now accounting for 45% of total lodging demand year-to-date.

Read in Spanish: Research and Analytics Update - October 09, 2024